Nov 16 (Reuters) – Some of the Wall Street banks that helped General Electric Co (GE.N), Toshiba Corp (6502.T) and Johnson & Johnson (JNJ.N) become massive conglomerates through acquisitions over the years are now profiting from their break-ups, a Reuters analysis showed.

The three companies, which in recent days announced plans to spin off divisions, doled out hundreds of millions of dollars in fees to banks, including Goldman Sachs Group Inc (GS.N), JPMorgan Chase & Co (JPM.N) and UBS Group AG (UBSG.S), to advise them on acquisitions over the years. Now, the same banks are getting paid to undo the outcomes of those deals.

Spokespeople for Goldman Sachs, JPMorgan and UBS did not respond to requests for comment.

While it’s not uncommon for an investment bank to advise a company on a spin-off after previously working on the company’s acquisitions, the spate of high-profile spin-offs by companies in recent days shines new light on the practice.

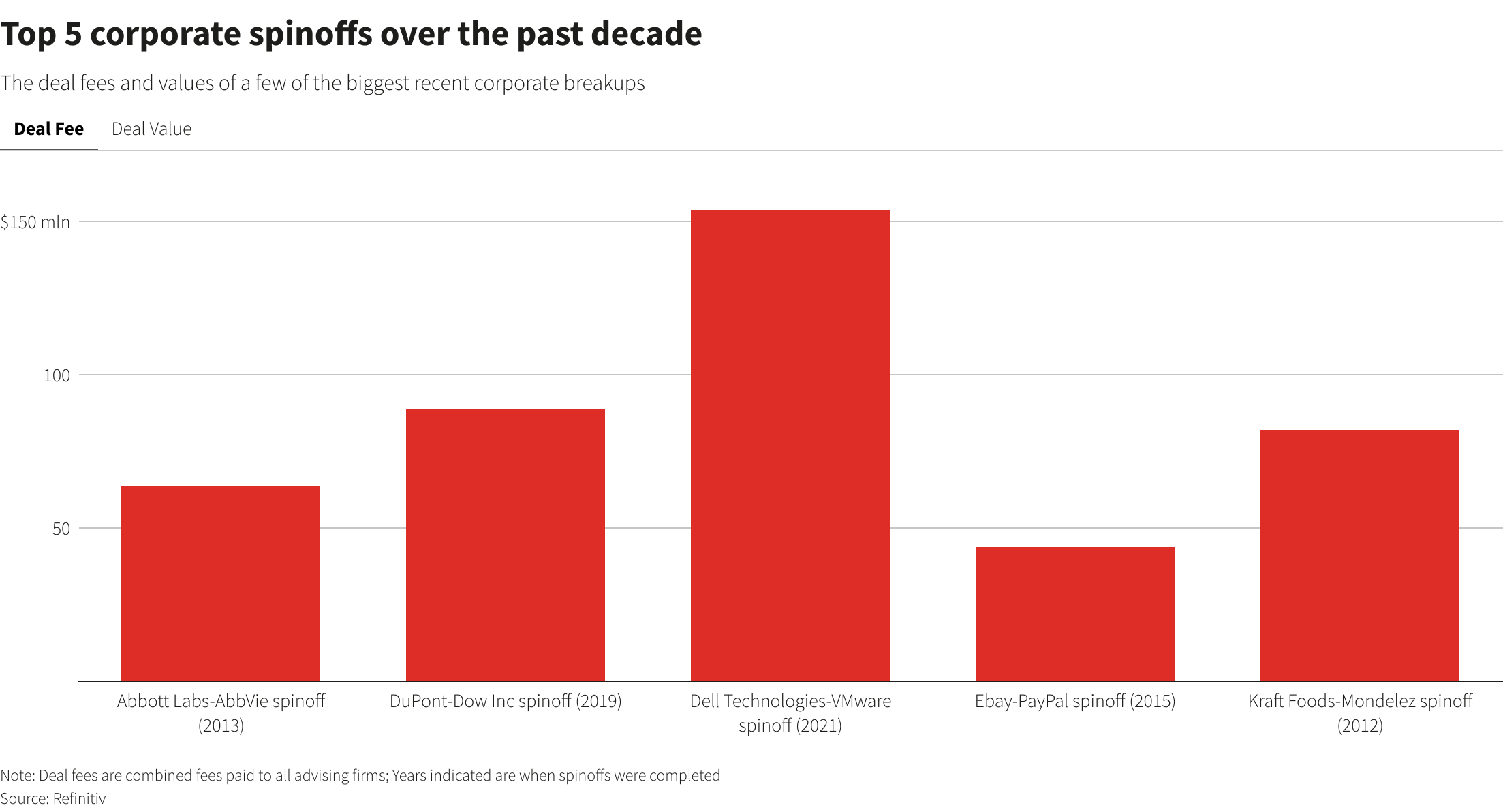

Banks have so far earned over $1 billion on spin-offs globally so far this year, nearly twice what they earned in 2020, according to Refinitiv.

Investors in those companies are not assured similar riches. Shares of companies that engage in acquisitions or divestments have had a mixed track record, often underperforming peers in the last two years, according to Refinitiv.

Erik Gordon, a professor of law and business at the University of Michigan, said banks do not generally break any rules when working on these deals because they are carrying out their clients’ wishes. But he noted that this did not absolve banks of the responsibility to advise against a deal they view as not in a company’s long-term interest.

“If the bankers deserve criticism, it is for not pushing back against a CEO who pushes a bad deal,” Gordon said.

In the case of GE, Goldman Sachs was one of the banks, alongside Evercore Inc (EVR.N), PJT Partners Inc (PJT.N) and Bank of America Corp (BAC.N), that stand to collect tens of millions of dollars from advising on the company’s break-up, according to estimates from M&A lawyers and bankers.

Goldman Sachs had previously collected nearly $400 million in fees advising the company on acquisitions, divestitures and spin-offs since 2000, making it GE’s top adviser based on M&A fees collected, according to Refinitiv.

JPMorgan, which advised J&J on its planned break-up, had previously made $206 million in fees since 2000 advising it on deals, according to Refinitiv. UBS, which worked on Toshiba’s break-up, had collected $12 million in fees, the Refinitiv data showed.

Industrywide, Goldman Sachs has earned the most in fees from advising on corporate break-ups thus far in 2021, followed by JPMorgan and Lazard Ltd (LAZ.N), according to Dealogic.

Corporate break-ups are on the rise amid a growing consensus on Wall Street that companies perform best only if they are focused on adjacent business areas, as well as increasing pressure from activist hedge funds pushing them in that direction.

Some 42 spin-offs collectively worth over $200 billion have been announced globally so far this year, up from 38 spin-offs worth roughly $90 billion in 2020, according to Dealogic. Investment banks have collected more than $4.5 billion since 2011 advising on spin-off deals globally, the Dealogic data shows.

For an interactive graphic, click on this link: https://tmsnrt.rs/3cgKJ9M

INDEPENDENT ADVICE

Investment bankers often argue that companies did not necessarily get it wrong when they embarked on deals they later reversed, because some combinations do not make sense forever.

Changes in a company’s technological and competitive landscape or in the attitude of its shareholders can push it to change course.

For example, GE shareholders were initially supportive of its empire-building acquisitions in businesses as diverse as healthcare, credit cards and entertainment in the 1990s, viewing them as diversifying its earnings stream. When some of these businesses started to underperform and GE’s valuation suffered, investors lost faith in the company’s ability to run disparate businesses.

Bankers also argue that most companies want to pay bankers for delivering deals rather than advice on whether they need to do a deal in the first place. This creates incentives for bankers to try to clinch a transaction rather than encourage a better outcome for their client that may not involve a deal.

But it also offers ammunition to Wall Street critics who argue that companies cannot rely on banks for independent advice on whether they should pursue a deal.

“Companies should develop valuations in house and with help from unbiased third-party advisers, whether or not they also hire an investment bank,” said Nuno Fernandes, professor of finance at IESE Business School.

Reporting by Anirban Sen in Bengaluru and David French in New York; Editing by Greg Roumeliotis and Stephen Coates

Our Standards: The Thomson Reuters Trust Principles.