There’s no doubt that money can be made by owning shares of unprofitable businesses. For example, biotech and mining exploration companies often lose money for years before finding success with a new treatment or mineral discovery. But while the successes are well known, investors should not ignore the very many unprofitable companies that simply burn through all their cash and collapse.

So should Keypath Education International (ASX:KED) shareholders be worried about its cash burn? For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. Let’s start with an examination of the business’ cash, relative to its cash burn.

Check out our latest analysis for Keypath Education International

When Might Keypath Education International Run Out Of Money?

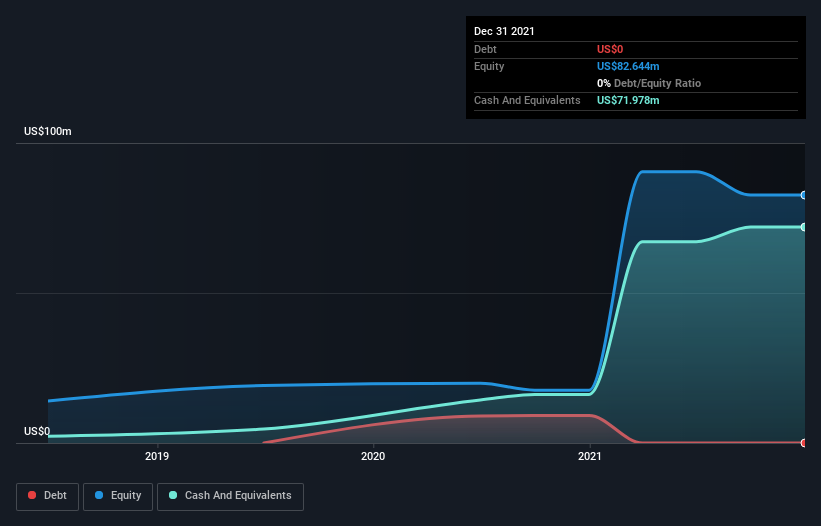

A company’s cash runway is calculated by dividing its cash hoard by its cash burn. When Keypath Education International last reported its balance sheet in December 2021, it had zero debt and cash worth US$72m. In the last year, its cash burn was US$11m. That means it had a cash runway of about 6.6 years as of December 2021. Notably, however, analysts think that Keypath Education International will break even (at a free cash flow level) before then. In that case, it may never reach the end of its cash runway. Depicted below, you can see how its cash holdings have changed over time.

How Well Is Keypath Education International Growing?

One thing for shareholders to keep front in mind is that Keypath Education International increased its cash burn by 939% in the last twelve months. While that certainly gives us pause for thought, we take a lot of comfort in the strong annual revenue growth of 56%. In light of the data above, we’re fairly sanguine about the business growth trajectory. Clearly, however, the crucial factor is whether the company will grow its business going forward. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

How Hard Would It Be For Keypath Education International To Raise More Cash For Growth?

While Keypath Education International seems to be in a decent position, we reckon it is still worth thinking about how easily it could raise more cash, if that proved desirable. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash and fund growth. We can compare a company’s cash burn to its market capitalisation to get a sense for how many new shares a company would have to issue to fund one year’s operations.

Keypath Education International has a market capitalisation of US$243m and burnt through US$11m last year, which is 4.5% of the company’s market value. Given that is a rather small percentage, it would probably be really easy for the company to fund another year’s growth by issuing some new shares to investors, or even by taking out a loan.

Is Keypath Education International’s Cash Burn A Worry?

As you can probably tell by now, we’re not too worried about Keypath Education International’s cash burn. In particular, we think its revenue growth stands out as evidence that the company is well on top of its spending. While we must concede that its increasing cash burn is a bit worrying, the other factors mentioned in this article provide great comfort when it comes to the cash burn. One real positive is that analysts are forecasting that the company will reach breakeven. After taking into account the various metrics mentioned in this report, we’re pretty comfortable with how the company is spending its cash, as it seems on track to meet its needs over the medium term. An in-depth examination of risks revealed 1 warning sign for Keypath Education International that readers should think about before committing capital to this stock.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies, and this list of stocks growth stocks (according to analyst forecasts)

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.