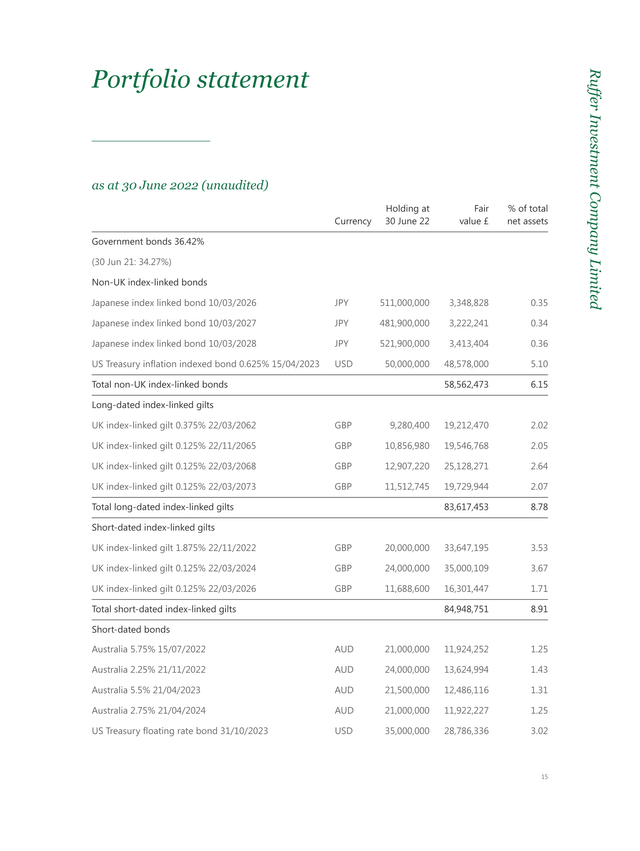

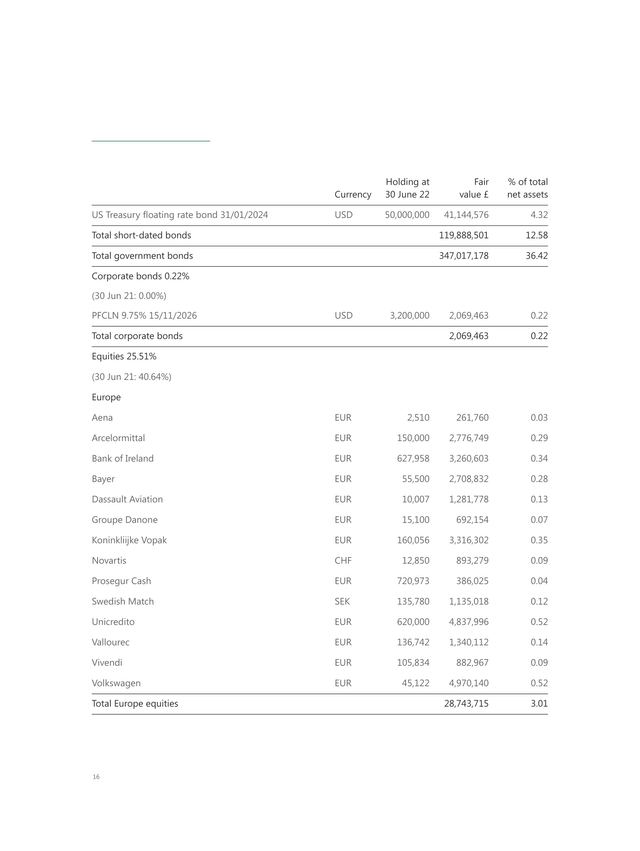

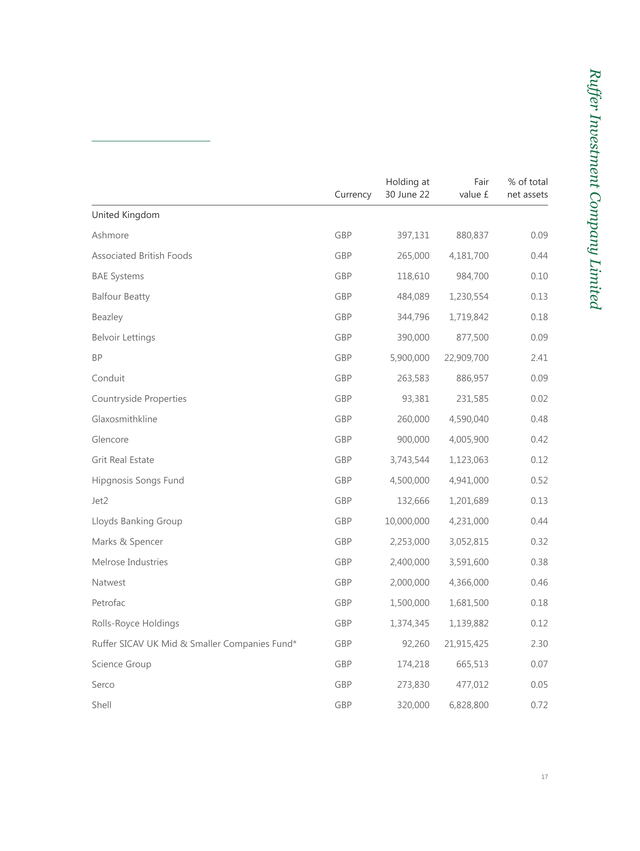

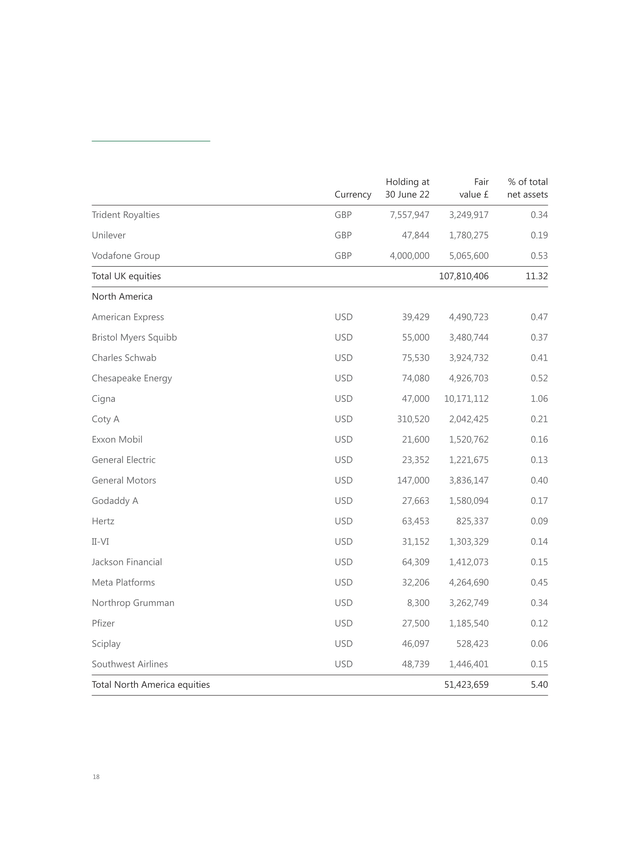

Key performance indicators

| 30 June 22 % | 30 June 21 % | |

|

Share price total return over 12 months1 |

5.6 |

19.5 |

|

NAV total return per share over 12 months1 |

5.9 |

15.3 |

|

Premium/(discount) of share price to NAV |

1.7 |

2.0 |

|

Dividends per share over 12 months2 |

3.05p |

1.90p |

|

Annualised dividend yield3 |

1.0 |

0.7 |

|

Annualised NAV total return per share since launch1 |

7.7 |

7.9 |

|

Ongoing charges ratio4 |

1.07 |

1.08 |

Financial highlights |

||

| 30 June 22 |

30 June 21 |

|

|

Share price |

300.00p |

287.00p |

|

NAV |

£952,784,773 |

£575,913,008 |

|

Market capitalisation |

£969,008,292 |

£587,541,854 |

|

Number of shares in issue |

323,002,764 |

204,718,416 |

|

NAV per share5 |

294.98p |

281.32p |

- Assumes reinvestment of dividends

- Dividends paid during the period

- Dividends paid during the year divided by closing share price

- Calculated in accordance with AIC guidance

- NAV per share as released on the London Stock Exchange

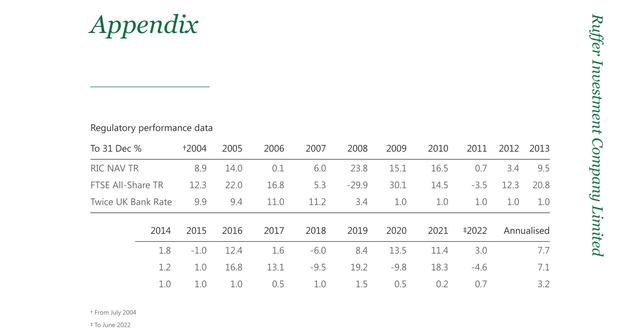

Source: RAIFM Ltd, FTSE International (FTSE). Data to June 2022. All figures include reinvested income. Ruffer performance is shown after deduction of all fees and management charges. Performance data is included in the appendix.

Investment Manager’s report – Performance review

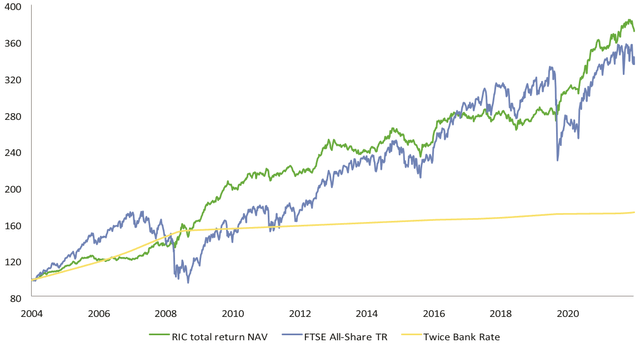

For the year to 30 June 2022 the company had a share price total return of 5.6% and the NAV total return of 5.9%. The Company has achieved its objective of preserving and growing shareholder capital.

The annualised NAV total return since inception of the Company in 2004 is 7.7%, which is ahead of UK equities with a much lower level of volatility and drawdowns.

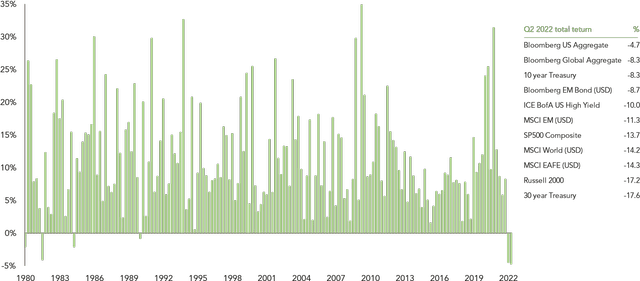

The period has been unusually challenging for investors. The below shows the returns an investor would have earned each quarter if they had had perfect foresight and could choose in advance to be in the best asset class. The remarkable thing about Q1 2022 is that the best-case scenario was a loss of 4.5% offered by US high yield bonds. History shows how rare it is that there was nowhere to hide. However, this wasn’t an anomaly – the second quarter was worse. The 60/40 portfolio is down 16% so far in 2022, a clear indicator that balanced, multi-asset portfolios are struggling.

BEST QUARTERLY TOTAL RETURN ACROSS ASSET CLASSES

Source: Bianco Research, FactSet, Reuters Datastream

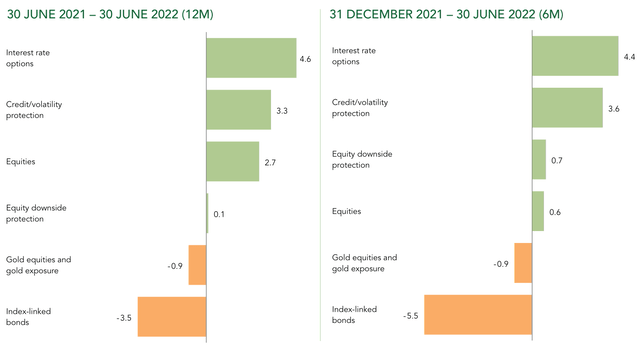

Given all that has happened year to date, we have presented contributions for the full year to 30 June 2022 and also for the first six months of 2022.

Performance contributions for six months to 30 June 2022

With nowhere to hide in conventional assets, it is no surprise that it was the portfolio’s unconventional protective assets that drove performance in the first six months of the year. Option protection via the Ruffer Protection Strategies Fund added 4.4%, driven mostly by interest rate options and equity puts. Credit protection continued to be an essential hedge contributing 3.6% via the Ruffer Illiquid Multi-Strategies Fund.

Within equities, energy stocks were the strongest contributors, adding 2.0% to performance.

Individual stock performance of note came from value cyclicals – for instance Chesapeake Energy (+31%) and Mitsubishi UFJ Finance (+19%). The decision to rotate into defence and healthcare stocks was also rewarded as Northrop Grumman (+29%) and Bristol Myers Squibb (+27%) performed well.

Towards the end of the period, as fears of recession grew, exposure to the auto manufacturing sector was hit hard with Volkswagen (-25%) and General Motors (-45%) together costing the portfolio -0.5%. In the UK, exposure to domestic value stocks via Ruffer UK Mid & Smaller Companies Fund (-14%) was hurt by the political omnishambles, inflation and recession risk, detracting -0.4% from the portfolio. Both cases provided a stark reminder that cheap stocks can get cheaper in the short term.

The carnage in the long-dated inflation-linked bond market should not be understated. These assets cost the portfolio -6.0%. The 2073 index-linked bond was down as much as 54% from its November 2021 all-time high – further commentary below.

Performance contributions for 12 months to 30 June 2022

The drivers of performance over 12 months were similar to those shaping the first half of 2022.

The toolkit of unconventional protections performed exactly as desired. Options added 3.7% and Ruffer Illiquid Multi-Strategies Fund added 3.3%. These protections provided both negative correlation and duration at a time of market stress and high cross-asset correlation in conventional markets.

Energy equities added 2.8% to performance and we took significant profits during the period. In the summer of 2021, we had a 7% allocation to these stocks at the end of the period this was closer to 4%.

Gold exposure and gold equities cost the portfolio 0.9% during the period. The largest individual pain came from Kinross Gold (-0.4%), which was the largest exposure in the portfolio to Russian asset risk. Gold is a prime example of the failure of conventional safe havens in recent times. Despite inflation and war being front page news, gold has misfired. We still think it has a valuable role to play, but this greater correlation with risk assets is a consequence of gold’s increased financialisation.

In the period, inflation-linked bonds cost the portfolio 3.5%, with the longest dated 2073 issue down 51%. We have long called these assets the ‘crown jewels’ in our portfolio due to our conviction that they should provide the perfect protection in the world of financial repression we are entering. We are still of this view. But the sensitivity to rising rates we have warned about, has now been felt. This illustrates a distinction we have been labouring; investing for inflation and investing for inflation volatility are not the same thing and conflating the two will be costly.

Mr. Market will make us crawl through fire for the gift of redemption, and derivative protection via the unconventional toolkit remains essential to safely navigating choppy and dangerous markets. Inflation-linked bonds are now back to pre-Brexit prices – and yet in our assessment the likelihood and proximity of the inflationary denouement is much greater.

Portfolio changes

In the last few months of the period, we reduced the risk in the portfolio, moving into what we call ‘crouch mode’ for what we believe will be a particularly dangerous period in the second half of this year. This de-risking included

- Reducing equities to a 25% weighting with hedges on top for good measure – this is the lowest weighting for Ruffer portfolios since 2003.

- Increasing portfolio duration as the rise in bond yields has increased its potential effectiveness as a hedge

- Rotating gold exposure from equities to bullion.

Investment outlook

Summary

- The long term – an era of inflation volatility

- The short term – the impossible tightrope walk

- The bear is mid-grizzle

- Hard hats on

There’s an old Charlie Munger quote: ‘If you’re not a little confused about what’s going on, you don’t understand it’.

That sums up the fog of war, literal and metaphorical, we find the global economy immersed in. We have never had higher conviction on the long term – that we have moved into a new regime of inflation volatility and those conventional portfolios are not going to fare well. In the short term, the outlook is far murkier and path-dependent as policymakers try to navigate a narrow path without either tipping the economy into a wage-price spiral or over the other side into recession. In the meantime, liquidity continues to drain from the system.

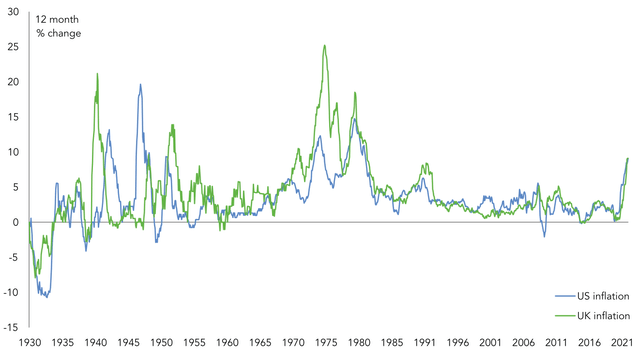

The long term – an era of inflation volatility

So what does the new regime look like? We think we return to spasmodic bouts of inflation volatility like we saw after the World War 2 period or indeed again in the 1970s. This long-term chart of UK and US inflation makes it clear that the last 30-40 years has been something of an aberration.

We expect an extended period of accelerating financial repression – where interest rates are below the rate of inflation, forcing negative real returns upon savers. ‘Stealing money from old people, slowly’ as Russell Napier has memorably described it. We believe we are evolving into a staccato, stop-start world of higher inflation and faster economic growth. This will be driven by targeted government stimulus to tackle the big societal issues of the day; inequality, climate change and now the containment of the geopolitical aspirations of China and Russia.

Source: Bank of England, ASR Ltd/ Refinitiv, data to June 2022

‘Ketchup inflation’

With these trends will come much greater economic and market volatility – the great moderation of inflation, growth and geopolitics enjoyed over the last 40 years is over. Having spent a decade trying in vain to create inflation, like an impatient child slapping on a ketchup bottle, central bankers have now got too much, all at once, in an uncontrolled splat. Inflation was desired as a palliative treatment for the system, the least painful method of debt default and wealth redistribution from old to young and rich to poor – but this ketchup inflation is too hot to handle.

The political imperative is that something must be done.

The short term – the impossible tightrope walk

Given that some inflation is desirable but too much is political suicide, perhaps the critical question is: how hard will central bankers fight inflation?

Monetary tightening is a little like going on a diet; easy to talk about and make detailed plans for, but difficult when it comes to the reality of the hard choices and abstinence.

From the current starting point of inflation at 40-year highs in both Europe and the US and a surging, fizzing jobs market – there are no good choices. Central bankers resemble quivering funambulists facing an impossible tightrope walk as they try to meet their objectives – full employment alongside low and stable inflation. Complicating matters further they have politicians breathing down their necks as inflation has spurred a cost of living crisis which now dominates the headlines.

On one side, tighten conditions too much and unemployment will surge, probably tipping the economy into recession and crushing asset markets. On the other side, do not tighten enough and risk inflation getting embedded into wages, beginning the dreaded wage-price spiral of previous inflationary episodes.

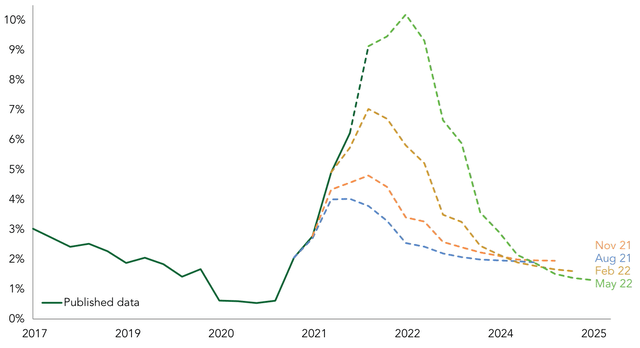

To make an impossible situation worse the tightrope walker appears a little short-sighted. This chart shows the Bank of England’s inflation forecasts and then the actual outturn (continuous green line) over the last year or so. In May 2021 the Bank of England thought inflation in summer 2022 would be around 2.5%. The actual result? 9.2%.

BANK OF ENGLAND MPC’S MODAL (BASELINE) CPI INFLATION FORECAST

Source: Bank of England, modal projections based on market pricing for Bank Rate over the forecast horizon

So, we must conclude that nobody has a clue – particularly not academic economists. Despite their recent mistakes they remain highly confident that inflation will drop back to around 2% by 2024 and stay there.

By June 2022, central bankers began the gradual process of rate rises in the UK and US. Indeed the Federal Reserve (FED) is engaging in the multi-variate experiment of simultaneous rate hikes and quantitative tightening.

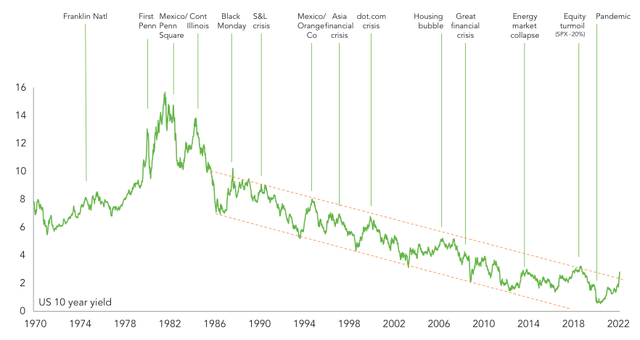

We are now starting to see what happens when more than a decade of easy money is removed from the system. As ex-Federal Reserve Governor Jeremy Stein said, ‘the thing about monetary policy is that it gets in all the cracks’. There is no hiding from the reality of higher interest rates. Every tightening cycle throughout history has ended with a recession, a market crisis or both. ‘The Fed hikes until something breaks’ as the old adage goes.

Source: FactSet

The punchbowl is being taken away. Quantitative easing is melting away and quantitative tightening is beginning. Combined with rapid-fire rate hikes, it’s a recipe for financial market sobriety.

It IS different this time

The policy reaction function has changed. For the last decade or so, downside risk was limited because investors knew that once equity markets declined 20% the Fed put would kick in and there would be policy easing. Today, given the need to dampen demand to tame inflation, the market upside is capped; rise too much and it will be met with more hikes and tighter financial conditions. The Fed wants higher risk premiums, and that means a lower market.

If it were to come, another Fed U-turn, similar to 2018’s Powell Pivot or last November’s abandoning the word “transitory”, would be confirmation central bankers have lost control and America has entered an era of structurally high inflation.

The Bezzle

The economist John Kenneth Galbraith coined the idea of ‘The Bezzle’, a form of psychic wealth that can be created by mistake or self-delusion. The theory goes that if a collector has a Picasso painting (or should it be an NFT these days?) worth $10 million and someone steals it, there is a period of time, potentially years, where both the collector and the thief believe they have a

$10 million asset and act accordingly. The effective wealth in their micro economy is $20 million. Half of the wealth that exists in this moment is illusory and will be destroyed only when the collector identifies the crime. Today’s bezzle is the trillions of dollars of assets held in crypto, profitless technology and venture capital funds globally. Although these sectors have felt significant pain already, we believe there is potentially much more to come as opacity, illiquidity and discretion around asset pricing allows the bezzle to be revealed slowly rather than with a bang.

The bear is only mid grizzle

How does an asset fall 95% in value? First it falls by 90% and then it halves!

Investors under the age of 60 have been conditioned to buy the dip. Central bank easing has always been just around the corner and the market recoveries are swift and steep. A look further back in history shows that the pattern many bear markets take is a steep drop, followed by a more prolonged, grind lower over a number of years. In these scenarios, buying the first downward lurch leaves your capital almost as impaired as buying at the top. Let me explain why we have high conviction that the bear market is not over, and stocks are not (yet) a buying opportunity.

The Fed is tightening into an economic slowdown.

Valuations have come down to something more reasonable but are based on earnings estimates that remain too optimistic, still forecasting growth when flat would be a good result.

Valuations have fallen because bond yields have risen, not because the equity risk premium has widened.

Earnings reflect record high margins at a time of rising debt service, labour and energy costs and supply chain disruptions.

Consumer and CEO confidence is at multi year lows, suggesting demand reduction and recession.

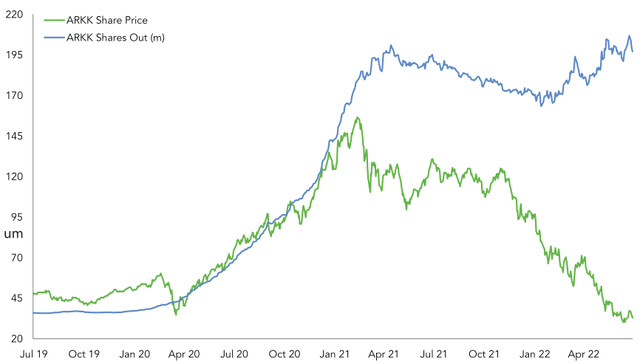

So far we have seen limited signs of capitulation. In fact, flows have remained strongly positive into equities throughout the sell-off. As the chart shows, ARK Innovation ETF has suffered no net redemptions despite declining 71% in price since the peak. The ‘buy the dip’ mentality is alive and well.

ARK INNOVATION ETF SHARE PRICE AND NUMBER OF SHARES OUTSTANDING

Source: Bloomberg, data to 30 June 2022

But the old rules no longer apply. Now that the cost of living crisis is front page news, the political imperative is to bring down inflation, not to support asset prices as in previous market sell-offs. Rather, we are in a negative feedback-loop, where any bear market rally sows the seeds of its own demise by loosening financial conditions, which in turn forces Central Banks to counteract.

Lastly, liquidity is the driver of market prices at the margin and this is likely to evaporate in coming months –as quantitative tightening takes hold, while rising short term rates creates a legitimate alternative to risky assets. The plumbing of the financial system exacerbates this liquidity squeeze by steering cash from banks to money market funds, which have less of a money multiplier effect in the economy. Banks, though not in danger, want to shed deposits and are not keen to expand their balance sheets, while money market funds reflect rate rises quickly and will attract flows.

Hard hats on!

In an episode of surprisingly and persistently high inflation, no allocation to risk escapes repricing. Investors in the Company delegate to Ruffer the task of assessing the economic and market landscape, evaluating the opportunity set and then deciding about how much risk to take.

We do not think this is a good environment to be risking our shareholders’ capital.

Rather, we see the coming months as a period to survive, given the extent of the uncertainty around the Ukraine war, central bank policy, inflation, corporate earnings and the consequences of rising interest rates.

This is all happening as the tide of easy money recedes, and we strongly suspect that some people will be found to have been swimming naked.

In this environment, an allocation to cash is an underrated decision – it provides the certainty of a slow erosion by inflation, but it also gives you the option value of being able to move quickly. This is clearly reflected in our portfolio construction.

As our CIO Henry Maxey wrote in the Ruffer Review at the turn of the year: ‘Winter is coming for liquidity, it’s coming for narcissism, it’s coming for crypto, it’s coming for retail punting, and it is definitely coming for businesses which depend on any of these things’.

There are times for a get rich portfolio and times for a stay rich portfolio. We believe this is the latter. There will be better moments and better prices in the future.

In The Science of Hitting by legendary baseball slugger Ted Williams, the key observation was that you don’t have to swing your bat at every pitch, only at the ones which look sufficiently attractive. That insight applies in spades to investing in risky assets at this juncture. We would rather lose half of our clients, than half of our client’s money.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

")